South Africa’s 2026 Budget Speech delivers a state of fiscal stability and significant adjustments, which, for property investors, makes a real difference.

There were no major new property taxes introduced, and several targeted adjustments were implemented that affect savings capacity, capital gains tax thresholds, retirement contributions, and long-term tax planning. For IGrow investors, these changes impact how portfolios are structured and how your wealth will grow effectively in 2026 and beyond.

Below is a breakdown of the Budget Speech adjustments that matter to property investors and savers.

1. OVERVIEW: THE OVERALL FISCAL POSITION

The 2026 Budget Speech in South Africa outlines the fiscal picture and the economic climate for the year ahead. Finance Minister Enoch Godongwana gave the 2026 Budget Speech on 25 February 2026. The core message conveyed was one of cautious optimism. Notably, South Africa has conquered its first debt stabilisation in 17 years and has secured its first credit rating upgrade in 16 years. The especially good news is that our nation has been removed from the FATF grey list. The overall mood is constructive and optimistic, even as the fiscal environment remains tight.

Key macro numbers:

- Real GDP (Gross Domestic Product) growth is projected at 1.6% for 2026, aiming to improve to an average of 1.8% over the medium term.

- The consolidated budget deficit was lowered to 4.5% of GDP in 2025/26, and falls even further to 4.0% in 2026/27

- The gross government debt stabilised at 78.9% of GDP in 2025/26, declining further to 77.3% in 2026/27. The primary budget surplus reached 0.9% of GDP in 2025/26, increasing to 1.6% in the coming year. (Source)

2. SAVINGS & INVESTMENTS: WHAT HAS CHANGED?

Several measures to be undertaken, as noted in the South African 2026 Budget Speech, influence savings structures and the ability to remain tax efficient, affecting taxpayers overall.

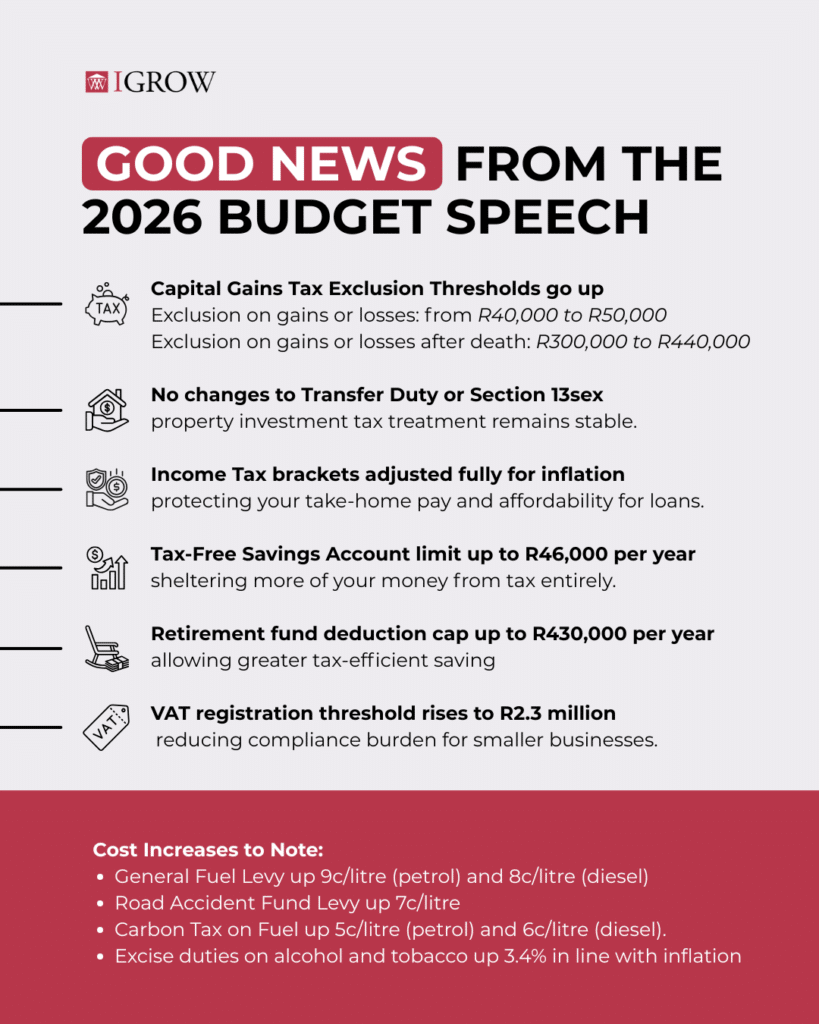

A. Tax-Free Savings Account (TFSA) Receives an Annual Limit Increase

The annual contribution limit for Tax-Free Savings Accounts has increased from R36,000 to R46,000. This is a substantial 27.8% increase. The lifetime limit hasn’t been officially confirmed in the budget speech, but it is expected to be reviewed. The TFSA limit increase in 2026 is an important adjustment that significantly reduces your tax burden.

Why does this matter for South African property investors?

IGrow Clients can now shelter a larger portion of savings away from income tax, capital gains tax (CGT), as well as dividends tax.

A TFSA is one of the few types of accounts that compound entirely tax-free over time. The increase in the yearly ceiling will promote wealth accumulation.

IGrow clients who have already maxed out their TFSA can now contribute an additional R10,000 per year, entirely tax-exempt.

For clients building their property deposits, or a buffer for times when there is a vacancy or higher maintenance costs, a TFSA used together with a property portfolio, uncovers a wonderful dual-asset-based wealth accumulation plan. (Source)

B. Retirement Fund Deduction Ceiling Cap Increase

The yearly cap on retirement fund deductions (including pensions, provident funds, and retirement annuity contributions) increases from R350,000 to R430,000 annually. This means high-income earners can shelter a larger portion of their income before tax year-end closes.

Why does this matter for property investors in South Africa?

Clients who have a high rental income or investment income can now add more contributions to their retirement funds in order to reduce their taxable income load.

A retirement annuity (RA) contribution of R430,000 each year at a 45% marginal tax rate incurs a tax saving of R193,500. This is a meaningful benefit.

For IGrow clients growing a property portfolio, this higher ceiling means you can adopt a stronger tax-efficiency plan. (Source)

3. PERSONAL INCOME TAX: BRACKET CREEP RELIEF

Personal income tax (PIT) brackets and rebates will be adjusted according to inflation for 2026/27. This is better news than many analysts expected. In previous years, only semi-relief was granted, and last year no adjustments were made, which effectively increased the tax burden on middle-income earners through what is known as fiscal drag or bracket creep.

The practical implications for IGrow clients:

- Employees earning a salary and self-employed investors will not lose disposable income due to bracket creep in 2026/27.

- This safeguards monthly cash flow for investors, which means you will have more capacity to sustain property investment contributions.

- There will be no changes to the Capital Gains Tax (CGT) inclusion rate or effective rates. This is important for clients planning to sell their investment properties.

There will be no changes to the corporate income tax rate (which remains at 27%). This is relevant for clients holding properties in (Pty) Ltd structures. (Source)

4. CAPITAL GAINS TAX (CTG) GENERAL ADJUSTMENTS

The CGT Property tax changes in the 2026 Budget Speech are:

Capital Gains Tax (CGT) – Annual Exclusion:

The annual exclusion for capital gains or losses has been increased from R40,000 to R50,000.

Exclusion on gains or losses after death: adjusted from R300,000 to R440,000.

Capital Gains Tax – Primary Residence Exclusion:

The exclusion applicable to capital gains or losses on the disposal of a primary residence has been increased from R2,000,000 to R3,000,000. (Source)

5. SMALL BUSINESS & COMPANY STRUCTURE RELIEF

For investors operating through companies or small businesses, certain structural thresholds were adjusted.

Two measures are particularly relevant for clients who own property through a company or small business structure:

A. VAT Registration Threshold Increase

The compulsory VAT registration threshold will increase from R1 million to R2.3 million in annual turnover. Small businesses (including property-related businesses) below this threshold are no longer required to register for VAT.

This is a significant measure that will aid small businesses below the VAT registration threshold. This is specifically significant for property investors with smaller-scale rental income portfolios or property management companies.

It will reduce your compliance burden and administrative overhead. These Property tax changes in 2026 are an uplifting factor to take into account for IGrow investors operating through small businesses. (Source)

B. Capital Gains Tax Exemption for Small Business Sales

The CGT exemption for the sale of a small business by an older person (55+ years old) increases from R1.8 million to R2.7 million. The qualifying business value ceiling will increase from R10 million to R15 million.

This is important for IGrow clients in their retirement planning who may be winding down business interests while continuing to hold onto property in the long-term. (Source)

6. AMENDMENT TO DONATIONS TAX EXEMPTION BETWEEN SPOUSES

According to Sanlam Investments, Section 56 of the Income Tax Act exempts donations between spouses from donations tax (at the moment). However, the government has noticed tax avoidance occurring between spouses staggering the cessation of their South African tax residency. In such cases, assets are transferred to a spouse who has already become a non-resident, which means the donation can qualify for the exemption.

The other spouse then ends their tax residency, reducing the income tax liability under the legislation: section 9H. This legislation means the couple can avoid both donations tax and the income tax on exit, in contrast to the intended outcome of the legislation. It was announced that, from 25 February 2026, the donations tax exemption will only be applied when the recipient spouse is a South African tax resident at the time of the donation. (Source)

7. WHAT WON’T CHANGE (REASSURANCE FOR INVESTORS)

Stability in the 2026 Budget Speech for South Africa is as relevant as reform/adjustments.

There are no changes to transfer duty, the Section 13sex Tax Act, or rental income tax treatment. The predicted R20 billion in additional tax measures from May 2025 has been withdrawn.

The following legislation remains unchanged, which is positive news for property investors:

- Transfer duty thresholds and rates – no changes are to take place.

- Section 13sex Tax Act allowances for residential rental properties- no changes.

- Corporate income tax rate- stays at 27%.

- Dividends withholding tax- remains unchanged.

- The predicted R20 billion tax increase from the May 2025 Budget has been withdrawn, due to better-than-anticipated SARS revenue collections.

This is a meaningful sign of fiscal stability and investor-friendly tax policy continuing. Property investors can plan and strategise with greater certainty. (Source)

8. MACRO ENVIRONMENT AND INFRASTRUCTURE INVESTMENT

Beyond direct tax measures, macroeconomic reforms influence long-term positions for South African property investors.

The broader macro and infrastructure context is relevant to property investors from a market perspective:

Public sector infrastructure spend will exceed R1 trillion over the medium-term timeframe, with noticeable allocations to transport, water, and energy. This affects the liveability and capital appreciation opportunities of residential property corridors.

Spatial and housing reforms are to take place: the government intends to restructure cities, increasing access to affordable housing near economic hubs. This supports the long-term benefit of urban residential property investment.

Energy reform is on the radar: regulatory changes have already unlocked significant private investment in generation capacity. Reduced loadshedding has improved rental property attractiveness and tenant retention rates.

The credit rating upgrade and South Africa’s removal from the FATF grey list improves South Africa’s investment risk profile. This provides a positive outlook for property investors, market sentiment and foreign investment. (Source)

9. INWARD FOREIGN LOANS FOR SOUTH AFRICAN RESIDENTS

Sanlam Investments staff note that, to encourage foreign trade and investments, the interest rate ceiling caps on inward foreign loans is going to be removed. This will take place if the loans are market-related and reported to the South African Reserve Bank (SARB).

Reducing Legislative Burden and Enhancing Competitiveness

To boost South Africa’s positioning as a financial and investment hub in Africa, the National Treasury aims to expand the HoldCo framework for corporates. This allows asset managers to manage foreign currency portfolios on a local level, not dissimilar to corporates.

This reform aims to create a “synthetic financial centre” with sights set on:

- Managing portfolios holding foreign assets, as well as

- Trading of foreign currency-denominated financial instruments.

This legislation aims to support greater participation in global capital trade, specifically for those with investments in Africa. The aim is also to bring in and mitigate foreign-based savings on behalf of South African investors. (Source)

Conclusion

The 2026 Budget Speech for South Africa pre-empts stability in the property tax environment, driving investor confidence.

There are no adverse CGT or transfer duty changes, alongside the positive outcome of the TFSA limit increase in 2026 and increased retirement deduction caps. This means investors have more space to optimise their tax efficiency.

For IGrow investors moving through these ongoing property tax changes in 2026, the message is clear. If you have a core strategy and remain compliant in your property investments, you will be supported within the current fiscal landscape. Now is the window to review/revise your property investment strategy and ensure your property portfolio is ready for the year ahead.

Contact an IGrow Investment Strategist today if you need to tweak your property portfolio strategy or improve tax efficiency. We are ready to turn your properties into a well-oiled investment vehicle destined for success.